What are the headlines?

Up until now, Corporation Tax has been set at a flat rate of 19%. From 01 April 2023, however, this is changing.

As outlined below, the changes revolve around business profits:

- Any profits up to £50,000 will be subject to Corporation Tax at 19%.

- Any profits above £250,000 will be subject to Corporation Tax at 25%.

- Any profits between £50,000 and £250,000 will be subject to a marginal rate, explained further below.

What do the changes mean for me?

A ‘small profits rate’ of 19% will be maintained, for companies with annual profits of up to £50,000. Hence, if your company has annual profits of £50,000 or less, you should see no change from the current rules.

On the other hand, the new 25% ‘main rate’ of Corporation Tax will only apply in full to those companies with profits of £250,000 or more. This has been intentionally done, so that smaller companies are not disproportionately affected by the changes.

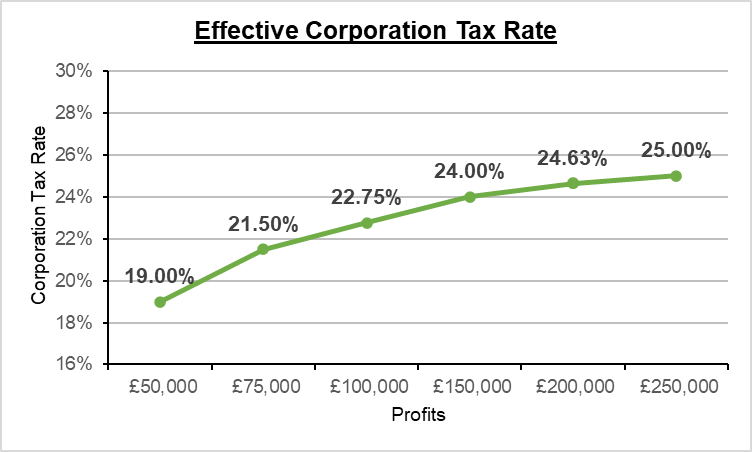

A marginal rate will apply for companies with profits between £50,000 and £250,000. The effect of this is that as total profits increase up to £250,000, the rate of corporation tax will do the same.

Effectively, this marginal rate is 26.5%. Whilst this may seem confusing at first, keep in mind that this will only apply to profits between £50,000 and £250,000 (i.e. it won’t be an ‘actual’ rate that the company pays, as illustrated in the below graph).

The end result is that as profit increases between these amounts, a greater proportion of profits are taxed at 26.5% rather than 19%, leading to the main rate of 25% being applied in full from the £250,000 profit mark onward.

So what happens around my company’s year-end date?

If a company’s accounting year-end date is 31 March, all is nice and simple – the changes will take effect from the start of the 23/24 accounting period.

In contrast, if a company’s accounting year straddles 01 April 2023, profit will be evenly time apportioned. For example – if the next year-end date is 31 May 2023, then the annual profits will be separated as follows:

- 10/12ths (Jun 22 to Mar 23)

- 2/12ths (Apr 23 to May 23)

The first ten months’ worth of profits will be subject to the ‘old’ rate of Corporation Tax (i.e. a flat 19%), whilst the final two months will be taxed according to the new rules.

What if I have more than one company?

The new rules will impact associated companies. Broadly speaking, two companies are ‘associated’ if at any given point in time (or within the 12 months prior):

- One company is in control of the other, or;

- Both companies are controlled by the same person, or group of persons.

Most commonly, ‘control’ is determined by a person’s shareholding and/or voting rights in a particular company. In some cases, the rights and ownership of others can be attributed to an individual when considering whether control exists. This usually applies between partners, though can also apply to certain other family members.

The impact of the new rules is that the taxable profit limits will be divided equally between any associated companies.

For example – if there are two associated companies, then the relevant thresholds for each will be £25,000 and £125,000 (below and above which, respectively, the Corporation Tax rates will be 19% and 25%).

The rules around associated companies (and the instances in which ‘control’ exists) can be complex. If you think they might apply to you, get in touch.